Ano após ano, o investimento em startups de tecnologia continua a crescer. Uma olhada no barômetro de startups da Bloomberg mostra um crescimento ridículo ao longo da última década . É difícil dizer se havia um momento melhor para abrir uma empresa de tecnologia (é bastante competitivo no momento). Porém, antes de mais nada você deve aprender sobre gestão de fluxo de caixa .

A gestão do fluxo de caixa é o processo de monitoramento, análise e otimização do valor líquido dos recebimentos de caixa menos os desembolsos de caixa. E, claro, na realidade, é mais difícil do que parece.

À medida que a indústria da tecnologia se fortalece, encontrando cada vez mais elementos das nossas vidas, a infra-estrutura da Internet melhora. Além disso, o hardware fica mais barato e os serviços em nuvem se expandem rapidamente; empreendedores tecnológicos ambiciosos são ideais para prosperar.

![Como gerenciar as finanças de uma empresa [guia definitivo]](http://monetize.info/wp-content/uploads/2020/08/How-To-Manage-The-Finances-Behind-A-Business-Ultimate-Guide.webp)

Índice

- 1 Erros de gerenciamento de fluxo de caixa

- 2 #1. Gastos excessivos

- 3 #2. Não usar um orçamento de fluxo de caixa

- 4 #3. Não manter uma reserva de dinheiro em mãos

- 5 #4. Confundindo lucro com o dinheiro que você ganha

- 6 #5. Esperando uma ascensão repentina ao sucesso

- 7 #6. Deixar de priorizar uma boa contabilidade

- 8 #7. Esquecendo a papelada

- 9 #8. A gestão inadequada de impostos

- 10 #9. Pagando suas responsabilidades antes do vencimento

- 11 #10. Não monitorar a saúde financeira de seus clientes

- 12 #11. Ignorando a natureza sazonal do negócio

- 13 #12. Não ter um plano de backup

- 14 Conclusão sobre erros de gerenciamento de fluxo de caixa

Erros de gerenciamento de fluxo de caixa

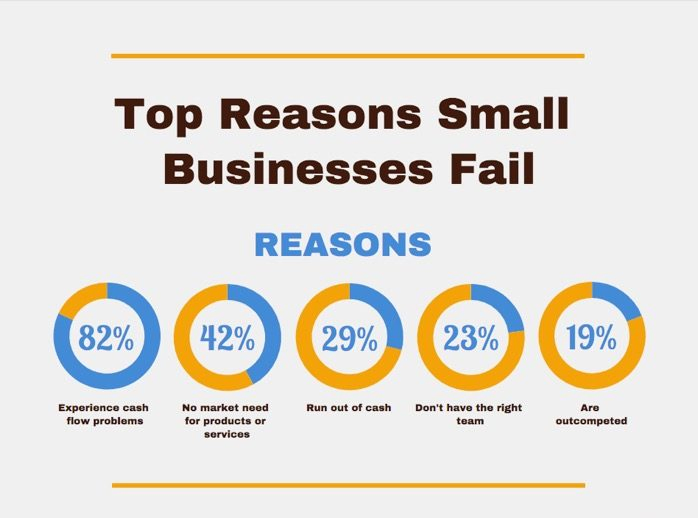

Os danos ao seu fluxo de caixa podem ser suficientes para afundar completamente o seu negócio, independentemente da escala da sua ideia ou da qualidade do seu trabalho, por isso você não pode se dar ao luxo de correr riscos.

Se você perceber que sua empresa gasta continuamente mais do que ganha, deve ficar claro que você tem um problema de gerenciamento de fluxo de caixa.

Aqui estão os erros mais comuns no gerenciamento de fluxo de caixa que podem matar seu negócio.#1. Gastos excessivos

Prejudicar seu fluxo de caixa é mais fácil por meio de gastos excessivos , e a maioria dos proprietários de startups cai nessa armadilha desde o início.

No entanto, existem outras razões pelas quais você pode gastar muito mais do que precisa. Pode ser que você seja imprudente e não preste atenção ao fato de que isso pode prejudicar o seu negócio, ou tenha a opinião de que para ganhar dinheiro é preciso gastar dinheiro.

Seja qual for o caso, alguma disciplina e planejamento não farão mal. Sem ele, você não pode proteger seu fluxo de caixa. A melhor forma de se tornar disciplinado e consciente dos seus gastos excessivos é analisar tudo e fazer uma lista de todos os seus gastos.

Depois disso, você poderia priorizar, decidir onde traçar os limites e se livrar de alguns deles. Somente o que for fundamental para suas operações futuras deverá permanecer.

#2. Não usar um orçamento de fluxo de caixa

Você deve definir expectativas realistas para vendas futuras. Você deve controlar os custos e fazer tudo o que puder para garantir que seus clientes paguem.

Essas mudanças por si só já deveriam fazer maravilhas para o fluxo de caixa de longo prazo da sua empresa. No entanto, você ainda pode descobrir que seu negócio está em uma situação difícil sem monitorar seu fluxo de caixa diário.

Para os varejistas, os meses imediatamente anteriores aos feriados são uma época em que o fluxo de caixa pode ser incrivelmente apertado. Você pode exigir mais estoque de seus fornecedores para se preparar para o fluxo de vendas, mas se esses pagamentos aos fornecedores chegarem antes de suas vendas acontecerem, você poderá ter problemas para pagar suas contas em dia. Durante este período, você pode considerar o financiamento de SR&ED como uma solução possível.

A utilização de um relatório de fluxo de caixa ajudará você a acompanhar as entradas e saídas de despesas de um determinado período. Deve ajudá-lo a prever quando terá mais dinheiro do que está entrando, para que possa planejar esses períodos problemáticos.

Sem ele, você está apenas se perguntando se terá o dinheiro quando precisar dele e provavelmente aumentará suas chances de enfrentar atrasos nos pagamentos e outras penalidades por contas vencidas.

#3. Não manter uma reserva de dinheiro em mãos

Não importa quantas reservas você tenha para proteger o caixa da sua empresa, as interrupções no fluxo de caixa são uma realidade empresarial.

Pode não fazer uma diferença considerável se você tiver uma reserva de poupança em mãos. No entanto, se sua empresa opera com saldo zero em conta, um mês lento de vendas pode significar um desastre instantâneo.

Se desejar proteger seu negócio de problemas de fluxo de caixa, você deve manter um saldo bancário que possa cobrir no mínimo três meses de suas despesas operacionais.

Dessa forma, mesmo que você encontre interrupções inesperadas no fluxo de caixa, você terá reservas para se proteger.

#4. Confundindo lucro com o dinheiro que você ganha

Nos negócios, geralmente é dada muita atenção aos lucros. No entanto, as empresas faliram muito antes de o resultado económico final aparecer na demonstração de resultados no final do ano, sem capacidade para pagar obrigações a fornecedores e salários a empregados.

Na demonstração de resultados você encontrará informações valiosas para analisar o desempenho do negócio. Infelizmente, isso não diz muito sobre se você está ganhando dinheiro.

Porém, a maioria dos empreendedores comete esse erro e foca apenas nos lucros.

Você também é um deles?

Talvez você já tenha pensado nisso. O conceito contábil de resultado econômico é diferente da categoria econômica de fluxo de caixa.

Lucro ou prejuízo é a expressão da diferença entre custos e receitas. O fluxo de caixa é a diferença entre receitas e despesas de caixa. As despesas não representam 100% das despesas, assim como as receitas na maioria das vezes não significam uma arrecadação imediata de dinheiro.

O lançamento zero na demonstração de lucros ou perdas é feito sobre os fornecimentos tributáveis da fatura emitida. No entanto, o dinheiro pode chegar até você com um atraso mais ou menos significativo.

Da mesma forma, o custo das faturas não significa necessariamente pagamento imediato. Por exemplo, o salário de dezembro faz parte do resultado econômico do ano.

Ainda assim, o pagamento (e, consequentemente, a diminuição do fluxo de caixa) só ocorrerá em janeiro do ano seguinte.

No caso de equipamento de escritório, computadores, linhas de produção, automóveis e edifícios, o desfasamento temporal é ainda mais pronunciado devido à distribuição da depreciação ao longo de vários anos, mesmo que já tenha pago há muito tempo por novos activos.

Custos, despesas e receitas podem diferir diametralmente na vida real e no resultado económico. A visão geral do fluxo de caixa mostra quanto dinheiro sai da empresa e quanto dinheiro teoricamente flui para dentro da empresa.

Você pode negociar com os clientes o pagamento posterior, embora já tenha pago suas entregas há muito tempo. Você não tem dinheiro, embora seja lucrativo.

A discrepância entre receitas e despesas deve forçá-lo a resolver ativamente a situação antes de receber a demonstração de resultados das contas.

#5. Esperando uma ascensão repentina ao sucesso

O mundo da tecnologia está repleto de exemplos de empresas que passaram de forma excepcionalmente rápida de quantidades desconhecidas para produtos quentes.

É assim que o investimento pode funcionar numa indústria tão especulativa: saber que a próxima ideia de um bilião de dólares (como o Snapchat) pode estar ao virar da esquina força os investidores a assumir riscos significativos, apoiando novos concorrentes.

O problema com isso é que as startups de tecnologia muitas vezes esperam seguir os passos dessas sensações noturnas, em vez de sonhar grande, priorizando o trabalho do dia a dia .

Você não abre uma empresa se não acredita na ideia, então essa crença (e alguma confiança) pode levá-lo a acreditar que seu sucesso é inevitável e que certamente virá em breve. Infelizmente, nem sempre é esse o caso.

Muitas startups tecnológicas com grandes ideias e grande potencial esgotam-se devido à má gestão ou mesmo ao mau timing – gastam descontroladamente, esperando fazer grandes progressos dentro de alguns meses. Depois encalharam porque nunca imaginaram que precisariam de um plano de crescimento plurianual.

#6. Deixar de priorizar uma boa contabilidade

Muitas startups, especialmente as novas, não conseguem compreender a importância de uma contabilidade confiável para cada transação que você faz. Ou eles entendem, mas pensam que não podem pagar.

Não existem pequenas transações e todas elas devem ser devidamente registradas. Dessa forma, a qualquer momento, você terá uma visão clara do seu negócio e do bem-estar financeiro da sua startup.

Informações organizadas sobre sua empresa devem estar à sua disposição a qualquer momento e será muito mais fácil acompanhar seu fluxo de caixa.

Afinal, o rastreamento de todos os recebimentos e transações deve facilitar a vida dos contadores externos caso você decida contratá-los.

#7. Esquecendo a papelada

Manter o controle da papelada é uma tarefa terrível para a maioria das pessoas, mas não fazê-lo pode causar problemas.

Seria melhor se você tivesse isso em mente, pois é mais provável que as agências governamentais prefiram lidar com empresas novas e pequenas que têm maior probabilidade de cometer erros nos documentos ou não preenchê-los.

As penalidades que se seguem a estas verificações são por vezes tão elevadas que o forçarão a reconsiderar se devem continuar com o seu trabalho. Mas mesmo que não seja, por que você deveria pagar se pode evitá-lo?

Além disso, certifique-se de ler e aprender sobre todos os recursos necessários para a conduta adequada do seu negócio e o que a legislação local exige.

#8. A gestão inadequada de impostos

Deve ser pago quando necessário. Mudanças repentinas nos impostos ou outros não pagamentos por parte do contribuinte podem afetar a saída de fundos.

Portanto, os impostos devem ser levados em consideração e, para tanto, devem ser feitos cálculos adequados no plano financeiro.

Assim, é necessário planejar qualquer uma dessas incertezas. Afinal, mais vale um pássaro na mão do que dois voando!

#9. Pagando suas responsabilidades antes do vencimento

As obrigações têm uma característica essencial. Eles têm uma certa maturidade. Significa que a obrigação de cumprir surgirá num ponto predeterminado no futuro.

Algumas obrigações são de natureza de curto prazo. Por exemplo, as obrigações para com os funcionários são geralmente pagas com um atraso de dez a vinte dias. Outros compromissos podem ser reembolsáveis durante um período mais longo. Por exemplo, a empresa reembolsará obrigações de empréstimos de longo prazo ao longo de vários anos.

Uma empresa financeiramente estável pode pagar suas dívidas quando elas estiverem vencidas. Não é justo pagar suas dívidas com atraso. No entanto, também é um erro pagar antecipadamente as obrigações gerais, ou seja, você pode ter encontrado os três princípios de todo empresário: comprar barato, vender por um preço alto e não pagar imediatamente.

É necessário capital de giro para financiar a operação. Você pode sacar seu valor a partir do valor do dinheiro associado ao estoque de materiais, mercadorias e produtos a receber da conta durante o ano e do dinheiro em sua conta e na tesouraria da empresa.

Esses ativos circulantes de curto prazo são constantemente convertidos de dinheiro em estoque, de estoque em contas a receber e de volta em dinheiro. O número de dias durante os quais o estoque e as contas a receber vinculam o caixa é a duração do financiamento operacional.

Para financiar o capital de giro por meio de vendas, o vencimento das obrigações deve ser idealmente igual ao prazo do financiamento operacional. Se você conseguir isso, sua empresa deverá se financiar .

Por outro lado, se as obrigações forem pagas em menos tempo do que você consegue financiar suas operações e receber o dinheiro das vendas, você precisará de outras fontes de financiamento, como um empréstimo operacional.

Se você concordou com os prazos para pagar suas obrigações, não faz sentido econômico pagá-las antes que elas cheguem.

#10. Não monitorar a saúde financeira de seus clientes

Um erro frequente na gestão do fluxo de caixa é não utilizar as economias decorrentes da eliminação de riscos associados a áreas-chave do seu negócio, como o volume de vendas ou o preço de compra de ativos fixos.

Pense nos possíveis riscos e encontre a sua causa raiz. Encontrá-lo pode consumir mais tempo do que apenas perceber um risco específico.

Porém, se o risco pode trazer consequências graves para o bolso da empresa, vale a pena fazer uma análise mais aprofundada dos motivos.

Por exemplo, você percebeu a ameaça potencial ao seu plano de fluxo de caixa devido a atrasos nos pagamentos aos seus principais clientes. Qual a razão deste comportamento dos seus parceiros de negócios?

Portanto, tente a análise financeira. A análise da solidez financeira e do desempenho da empresa do seu parceiro de negócios pode ser simplificada com um rápido teste de crédito. Baseia-se em vários números das demonstrações contábeis.

Graças aos resultados dos testes de crédito, você pode avaliar seus parceiros de negócios em uma escala de um a cinco. Ao planejar seu fluxo de caixa, você deve focar principalmente nos “quatros” e “cinco”, ou seja, para empresas que potencialmente não têm condições de pagar suas dívidas.

O risco de atrasos nos pagamentos dos clientes causados pelos seus graves problemas financeiros representa um elevado grau de ameaça ao seu fluxo de caixa. Graças ao teste de crédito, você deverá conhecer esse risco e, portanto, exigir, por exemplo, a entrega de mercadorias mediante pré-pagamento.

#11. Ignorando a natureza sazonal do negócio

As empresas que não têm operações anuais são ricas em caixa durante os períodos de pico e enfrentam dificuldades em gerir as saídas de caixa durante o resto do período.

Portanto, quando começa a temporada de riqueza, as pessoas tendem a assumir obrigações indiretas que se tornam difíceis de cumprir fora da temporada.

Para evitar essa má gestão do fluxo de caixa, você deve garantir reservas suficientes fora de temporada no plano financeiro.

#12. Não ter um plano de backup

As condições de mercado atuais são tais que você nem sempre está ciente do que acontecerá e para onde seu negócio está indo. Qualquer coisa pode dar errado a qualquer momento e você pode nem perceber.

Portanto, estar preparado para tais casos, mesmo que eles nunca aconteçam, é a maneira mais sábia e segura de salvar sua startup do fracasso. Ter alguns fundos de emergência que você possa usar é quase necessário e pode até afetar a falência ou a superação da situação com sucesso.

Existem várias maneiras de lidar com isso. Uma das melhores maneiras é ter uma conta poupança para depositar dinheiro de vez em quando. Acumular dinheiro dessa forma leva um pouco de tempo, mas é seguro e sem riscos.

Alternativamente, você pode obter uma linha de crédito, que é muito mais rápida, mas exige que você pague mais. No entanto, certifique-se de fazer isso apenas quando necessário.

Conclusão sobre erros de gerenciamento de fluxo de caixa

As questões de fluxo de caixa são um dos maiores desafios de possuir um negócio. No entanto, se você for objetivo em relação ao seu negócio, limitar gastos desnecessários e tomar cuidado com possíveis armadilhas, deverá estar muito acima de seus colegas de trabalho em termos de potencial para o sucesso comercial a longo prazo.

Começar uma startup exige muito esforço e força mental, e você inevitavelmente cometerá alguns erros, especialmente se for novo no negócio.

No entanto, alguns erros custam mais do que outros. Portanto, seria sensato observar o que outros proprietários de startups fizeram antes de você e tentar evitá-lo. Dessa forma, seu negócio terá muito mais chances de sobreviver nesse mercado já saturado!

Não importa quão incrível seja o seu plano de negócios, quão lucrativo você seja ou quantos investidores estejam interessados em apoiar o seu negócio, você não sobreviverá se não conseguir administrar seu fluxo de caixa.

Monetize.info é o melhor para startups e comunidades de pequenas empresas em qualquer lugar. Eu leio todos os dias e agora meu desempenho empresarial melhorou muito e estou muito grato por ter encontrado www.economicfy.com, que me ajudou a pagar minhas contas quando perdi meu emprego no meio da pandemia. Estes são meus dois melhores recursos e favoritos. Espero que estes dois sites ajudem alguns outros