Year after year, investment in tech startups continues to grow. One look at the Bloomberg startup barometer shows ludicrous growth over the last decade or so. It is hard to say if there was a better time to start a technology company (it is pretty competitive at the moment). However, before anything else you should learn about cash flow management.

Cash flow management is the process of monitoring, analyzing, and optimizing the net amount of cash receipts minus cash disbursements. And, of course, in reality, it is harder than it may sound.

As the technology industry gets stronger, finding its way into more and more elements of our lives, internet infrastructure gets better. Also, hardware gets cheaper, and cloud services expand rapidly; ambitious tech entrepreneurs are ideal for thriving.

![How To Manage The Finances Behind A Business [Ultimate Guide]](http://monetize.info/wp-content/uploads/2020/08/How-To-Manage-The-Finances-Behind-A-Business-Ultimate-Guide.webp)

Table of Contents

- 1 Cash Flow Management Mistakes

- 2 #1. Overspending

- 3 #2. Not Using A Cash Flow Budget

- 4 #3. Not Keeping A Buffer Of Cash On Hand

- 5 #4. Confusing Profit With The Money You Make

- 6 #5. Expecting A Sudden Rise To Success

- 7 #6. Failing To Prioritize Good Bookkeeping

- 8 #7. Forgetting About The Paperwork

- 9 #8. The Improper Management of Taxes

- 10 #9. Paying Your Liabilities Before They Are Due

- 11 #10. Not Monitoring The Financial Health Of Your Customers

- 12 #11. Ignoring The Seasonal Nature Of The Business

- 13 #12. Not Having A Backup Plan

- 14 Conclusion on Cash Flow Management Mistakes

Cash Flow Management Mistakes

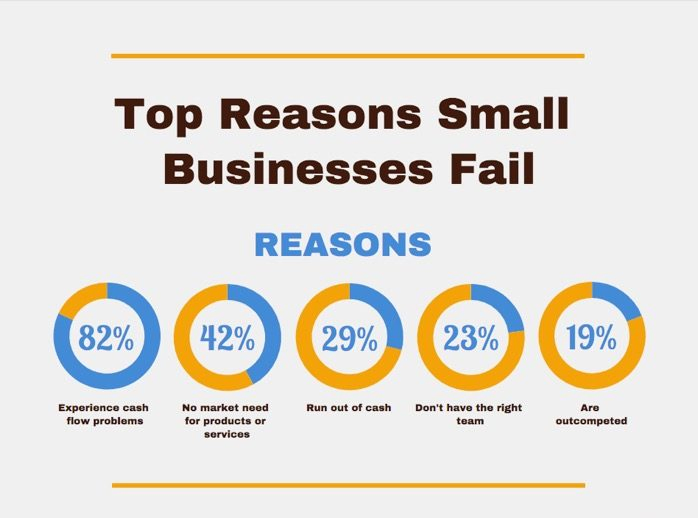

The damage to your cash flow can be enough to sink your business thoroughly, regardless of the scale of your idea or the quality of your work, so you can’t afford to take any chances.

If you see that your business is continuously spending more than it earns, then it should be clear that you have a cash flow management problem.

Here are the most common mistakes in cash flow management that can kill your business.#1. Overspending

Hurting your cash flow is easiest through overspending, and most startup owners fall into this trap early on.

However, there are other reasons why you can spend much more than you need to. It may be that you are reckless and do not pay attention to the fact that it can damage your business, or you have the opinion that to make money, you need to spend money.

Whatever the case, some discipline and planning won’t hurt. Without it, you can’t protect your cash flow. The best way to become disciplined and aware of your overspending is to analyze everything and make a list of all your expenses.

After that, you could prioritize, decide where you could draw the line, and get rid of some of them. Only what is fundamental to your future operations should remain.

#2. Not Using A Cash Flow Budget

You should set realistic expectations for future sales. You should reign in costs and do everything you can to make sure your customers pay.

These changes alone should do wonders for your company’s long-term cash flow. However, you may still find that your business is in a tight spot without tracking your daily cash flow.

For retailers, the months immediately before the holidays are a time when cash flow can be incredibly tight. You may require more inventory from your suppliers to prepare for the influx of sales, but if these payments to suppliers arrive before your sales happen, you may have trouble paying your bills on time. During this time, you may want to consider SR&ED financing as a possible solution.

The use of a report on the cash flow will help you keep track of the influx and outflow of expenses for a certain period. It should help you anticipate when you will have more money than is coming in, so you can plan for these problematic periods.

Without it, you are just wondering if you will have the money when you need it, and you will probably increase your chances of facing late payments and other penalties on overdue bills.

#3. Not Keeping A Buffer Of Cash On Hand

No matter how many reserves you have in place to protect your company’s cash, cash flow disruptions are a business reality.

It may not make a considerable difference if you have a cushion of savings on hand. However, if your company operates with a zero account balance, one slow month of sales can mean instant disaster.

If you wish to protect your business from cash flow problems, you should maintain a bank balance that can cover a minimum of three months of your operating expenses.

This way, even if you encounter unexpected cash flow disruptions, you have reserves to protect yourself.

#4. Confusing Profit With The Money You Make

In business, much attention is usually paid to profits. However, companies went bankrupt long before the final economic result appeared in the income statement at the end of the year without the ability to pay obligations to suppliers and wages to employees.

In the income statement, you will find valuable information for analyzing business performance. Unfortunately, this doesn’t say much about whether you are making money.

However, most entrepreneurs make this mistake and focus only on profits.

Are you one of them, too?

Maybe you have already thought about it. The accounting concept of an economic result is different from the economical category of cash flow.

Profit or loss is the expression of the difference between costs and income. Cash flow is the difference between cash income and expenses. Expenses do not account for 100% of expenses, just as income most often does not mean an immediate collection of money.

Zero entry in the statement of profit or loss is entered on the issued invoice’s taxable supplies. However, the money may come to you with a more or less significant time lag.

Similarly, the cost of the invoices does not necessarily mean immediate payment. For example, the salary for December is part of the economic result of the year.

Still, the payment (and, consequently, the decrease in cash flow) will not occur until January of the following year.

In the case of office equipment, computers, production lines, cars, and buildings, the time lag is even more pronounced due to the spread of depreciation over several years, even though you have long paid for new assets.

Costs, expenses, and income can differ diametrically in real life and the economic outcome. The cash flow overview shows how much money flows out of the company and how much money theoretically flows into the company.

You can negotiate with customers for later payment, while you had already paid for your deliveries a long time ago. You have no money, even though you are profitable.

The discrepancy between income and expenses should force you to actively resolve the situation before receiving the accounts’ income statement.

#5. Expecting A Sudden Rise To Success

The tech world is replete with examples of companies that have moved exceptionally quickly from unknown quantities to hot goods.

It is how investing can work in such a speculative industry: knowing that the next trillion-dollar idea (like Snapchat) may be just around the corner forces investors to take significant risks by supporting new contenders.

The problem with this is that tech startups often expect to follow these late-night sensations in the footsteps instead of dreaming big by prioritizing day-to-day work.

You don’t start a company if you don’t believe in the idea, so that belief (and some confidence) can lead you to believe that your success is inevitable and sure to come soon. Unfortunately, this is not always the case.

Many tech startups with great ideas and great potential burn out because of poor management or even bad timing-they spend wildly, expecting to make great progress within a few months. Then they run aground because they never imagined they would need a multi-year growth plan.

#6. Failing To Prioritize Good Bookkeeping

Many startups, especially new ones, fail to understand the importance of reliable accounting for every transaction you make. Or they do understand but think they cannot afford it.

There are no small transactions, and that all of them must be properly registered. This way, at any time, you will have a clear view of your business and the financial well-being of your startup.

Organized information about your company should be at your disposal at any given time, and it will be much easier for you to keep track of your cash flow.

After all, tracking all receipts and transactions should make it easier for external accountants if you decide to hire them.

#7. Forgetting About The Paperwork

Keeping track of paperwork is a terrible task for most people, but failing to do so can leave you in trouble.

It would be better if you had this in mind, as it is more likely that government agencies prefer to deal with new and small businesses that are more likely to make mistakes in the documents or fail to fill them out.

The penalties that follow these checks are sometimes so high that it will force you to reconsider whether you should continue with your work at all. But even if it isn’t, why should you pay if you can avoid it?

Also, ensure that you read and learn about all the features necessary for your business’s proper conduct and what your local legislation requires.

#8. The Improper Management of Taxes

It should be paid when necessary. Sudden changes in taxes or other non-payments on the part of the taxpayer may affect the outflow of funds.

Therefore, taxes should be taken into account, and for this purpose, appropriate calculations must be made in the financial plan.

Thus, it is necessary to plan for any of these uncertainties. After all, a bird in your hand is worth two in the bushes!

#9. Paying Your Liabilities Before They Are Due

Obligations have one essential feature. They have a certain maturity. It means that the obligation to perform will arise at a predetermined point in the future.

Some obligations are of a short-term nature. For example, obligations to employees are usually repaid with a delay of ten to twenty days. Other commitments may be repayable over a longer period. For example, the company will repay obligations from long-term loans over several years.

A financially stable company can pay its debts when they are overdue. It is not fair to pay your debts late. However, it is also a mistake to pay off general obligations early, i.e., you may have encountered the three principles of every business person-buy cheap, sell at a high price, and not pay immediately.

Working capital is required to finance the operation. You can withdraw its amount from the value of the money associated with the inventory of materials, goods, and products account receivable during the year and the money in its account and the company’s treasury.

These current short-term assets are constantly converted from money to inventory, from inventory to receivables, and back to money. The number of days during which inventory and accounts receivable link cash is the duration of operational financing.

To finance working capital through sales, the obligations’ maturity should be optimally equal to the term of operational financing. If you can achieve this, your company should finance itself.

Conversely, if the obligations are to be repaid in less time than you can finance your operations and receive money from sales, you will need other financing sources, such as an operating loan.

If you have agreed on deadlines for paying your obligations, it makes no economic sense to pay them before they come.

#10. Not Monitoring The Financial Health Of Your Customers

A frequent mistake in cash flow management is not to use the savings that arise from eliminating risks associated with key areas of your business, such as sales volume or the purchase price of fixed assets.

Think about the possible risks and find their root cause. Finding it can be more time-consuming than just realizing a particular risk.

However, if the risk can have severe consequences for the company’s wallet, it is worth conducting a deeper analysis of the reasons.

For example, you have realized the potential threat to your cash flow plan due to delays in payments to your main customers. What is the reason for this behaviour of your business partners?

Therefore, try financial analysis. Analyzing your business partner’s company’s financial strength and performance can be simplified with a quick credit test. It is based on several figures from the accounting statements.

Thanks to the credit test results, you can rate your business partners on a scale of one to five. When planning your cash flow, you should focus mainly on the” fours” and “fives,” that is, for companies that are potentially unable to pay their debts.

The risk of late payments by customers caused by their severe financial problems poses a high degree of threat to your cash flow. Thanks to the credit test, you should know this risk and therefore require, for example, the delivery of goods under prepayment.

#11. Ignoring The Seasonal Nature Of The Business

For businesses that do not have annual operations are cash-rich during peak business seasons and face difficulties managing cash outflows during the remainder of the period.

Therefore, when the season of rich money begins, people tend to take on overhead obligations that become difficult to cope with in the off-season.

To avoid such poor cash flow management, you should ensure enough off-season reserves in the financial plan.

#12. Not Having A Backup Plan

Market conditions today are such that you may not always be aware of what will happen and where your business is going. Anything can go wrong at any moment, and you may not even notice it.

Therefore, being prepared for such cases, even if they never happen, is the wisest and safest way to save your startup from failure. Having some emergency funds that you could use is almost necessary, and it may even affect whether you go bankrupt or get through it successfully.

There are several ways to deal with this. One of the best ways is to have a savings account to deposit money from time to time. Accumulating money in this way takes a little time, but it is risk-free and safe.

Alternatively, you can get a line of credit, which is much faster but requires you to pay more. However, ensure that you only do this when necessary.

Conclusion on Cash Flow Management Mistakes

Cash flow issues are one of the biggest challenges of owning a business. However, if you are objective about your business, limit unnecessary spending, and beware of potential pitfalls, you should be way above your business colleagues in your potential for long-term business success.

Starting a startup takes a lot of effort and mental strength, and you inevitably will make a few mistakes, especially if you are new to the business.

However, some mistakes cost you more than others. Therefore, it would be wise to observe what other startup owners have done before you and try to avoid it. This way, your business should have a much better chance of surviving in this already saturated market!

No matter how incredible your business plan is, how profitable you are, or how many investors are interested in supporting your business, you will not survive if you can’t manage your cash flow.

Monetize.info is the best for startups and small businesses community anywhere. I read it every day and now my business performance have improved a lot and I’m so grateful I found www.economicfy.com , it helped me pay my bills when I lost my job on the middle of pandemic. These are my best two favorite and resources. Hope this two sites helps some others